The Future of Money: a Digital Currency Primer

Q3 | September 2021

Topic: Investments

September 23, 2021

Image used with permission: iStock/alexsl

Download This Issue

Download this full issue of Nexus Notes QuarterlyOn a Side Note…

See another Investments Nexus Notes Quarterly article that may be of interest to you.

Why Scary Headlines and Strong Returns Can Coexist – and What Your Brain Gets Wrong About Both

The Future of Money: a Digital Currency Primer

Q3 | September 2021

As a bottom-up investment management firm, we spend a lot of time looking at specific companies. But keeping an eye on evolving industry trends can be just as important. The shift to digital currencies is one such trend, and in this instance it’s a trend that’s likely to have implications for all of us.

While the first Bitcoin was created in 2009, it is only in the last five years that crypto currencies have become a hot topic. With their promise of revolutionizing the way the world thinks of both currency and payments, individuals, corporations and central banks are working hard to map out the future of money. Just last month the country of El Salvador introduced Bitcoin as an official currency. Other efforts include Facebook’s failed, fully-backed digital currency Libra, as well as China’s recently launched digital Yuan.

The intention of this blog is to cover, at a very high level, some of the basics that are required to better understand digital currencies. Hopefully it will help you to make sense of the headlines and developments that we are sure will continue to come our way.

On the surface, a “digital currency” feels like a small jump from where we are today with digital banking. Transactions like automatic deposits, e-transfers, and mobile payments mean that funds come and go without physical money ever exchanging hands. You can pay for your Starbucks with your watch, and you can even authorize Nexus to pull a transfer directly from your bank account! When we step back and consider how much has changed thanks to digital banking, it truly is amazing. But digital currencies are a quantum leap beyond traditional banking. The major differences vary depending on the type of digital currency. So let’s take a look at some broad categories.

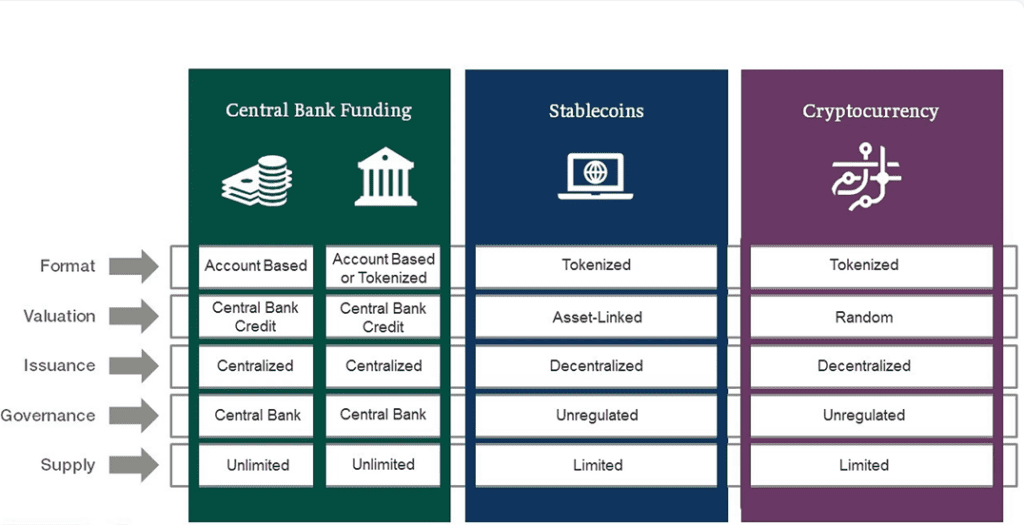

Digital currencies can be categorized into three distinct buckets: Cryptocurrencies, Stablecoins and Central Bank Digital Currencies.

Click on the video below to listen to Alana’s quick overview of some of the key differences of the various digital currencies.

Cryptocurrencies

Since the price of a Bitcoin went from under $10,000 to over $18,000 in December 2017, cryptocurrencies have been in the news and on people’s radar. Despite all this attention, many aspects of cryptocurrency still baffle us and others. For instance, blockchain technology, the anonymity associated with owning and trading in cryptos, the “mining” of new coins and the huge price swings unsettle people. For some, it’s all just a little bit too confusing, and, for others, cryptocurrencies simply don’t jive with their current understanding of currency or money. The way we see it, there are two camps of people who are currently involved in cryptos: those who value privacy and are willing to live with the volatility that comes with it, and those who enjoy the speculative nature that is a by-product of the large price swings. It won’t surprise you, but at Nexus we aren’t in either camp. We need to understand what drives valuation changes in our investments before we can be “adopters”.

Stablecoins

Like the cryptocurrencies described above, stablecoins are not controlled by a central bank. The exact attributes of stablecoins vary widely, but in contrast to cryptocurrencies which leave valuation to market supply and demand, stablecoins derive value from underlying assets which back their value. Because of this difference, stablecoins are designed to avoid the major price swings that are associated with cryptos (thus the name). But this change in pricing dynamic also shifts the profile of who might be interested in using/investing in such a currency. For some, the very appeal of a crypto is the lack of any tie to traditional fiat currencies.

There are several stablecoins already in the market, with the largest one being Tether. The value of one digital coin (TUSD) is pegged to the value of a US dollar, and the total market value is about $68 billion. But Tether and others face regulatory challenges and questions about the nature and quality of the assets that back their currencies. As mentioned above, Facebook’s Libra did not capture broad interest. But Facebook is refining its efforts to develop a stablecoin (now called Diem) that will no doubt integrate with the broad commercial aspects of the Facebook ecosystem (Instagram, WhatsApp, Facebook Marketplace, etc.).

Central Bank Digital Currencies (CBDCs)

Finally, there are the digital currencies issued by central banks (CBDCs). They are the most likely digital replacement of traditional money. Unlike cryptocurrencies and stablecoins, which avoid centralized oversight and prize anonymity, CBDCs are theoretically backed by fiat currencies and regulated by central banks.

Pressure on large central banks, such as the Federal Reserve and the European Central Bank, to get moving has been mounting because of China’s recent roll-out of the digital Yuan (a CBDC), as well as the increasing adoption of cryptos and stablecoins generally. Despite this pressure, there are no major CBDC launches expected for several years. Because CBDCs may eventually replace traditional money, central banks are moving cautiously. They are mindful of the potential disruption that CBDCs might generate. A successful digital currency will need to act like a cryptocurrency in some respects, such as providing easy settlement and efficient cross-border transfers. But it must also deliver the valued attributes of traditional money that many take for granted, like portability, anonymity and limited daily fluctuations in value.

It is apparent that the three digital currencies described above serve vastly different roles. While CBDCs are the most likely candidates to replace today’s currencies, it is possible that the future involves all three types of digital currencies described above.

As we consider the adoption of digital currencies, there are serious implications for security and privacy, as well as myriad other potential knock-on effects. Such effects are not confined to the traditional financial sector. The digitization of money will affect every corner of the economy. Below we list and briefly discuss a few issues to be weighed as we consider the next chapter in the history of money.

Privacy and security:

As with all things digital, digital currencies come with a heightened risk of cyber-attack. While blockchain has proven to be resilient against hacks, a CBDC solution will likely look different as it would not use a decentralized ledger system that comes with blockchain.

Decreased dependency on the US dollar:

Part of the dollar’s appeal is the safety net and portability that it provides. Many emerging economies either explicitly or informally operate on the strength and stability of the US dollar. Digital currencies could replace the role of the dollar in certain circumstances.

Possible shift in the role of traditional banks:

The role of commercial banks in deposit-taking, cash distribution and liquidity would be much different in an entirely digital system. For better or worse, developments in “fintech” technology and the digitization of currencies would broaden the number and nature of participants in the financial system. Uneven regulatory treatment will be a fundamental problem.

Public skepticism:

While we all know people who profess to fully understand the world of cryptocurrencies, we are skeptical that people will readily accept that their money is better off in a computer as opposed to under the mattress. As digital currencies become a little more common, we expect traditional currency and digital currency to co-exist for a long time. To our mind, full replacement of traditional currencies by digital ones is only a very distant possibility.

What do you think that the future of money will look like?